Market Update - May 2022

Buckle up- Rate rise ahead!

Say good-bye to cheap money!

Spearheading a jam packed week is the RBA monetary policy decision due today (3 May 2022). Many economists are predicting today to be the start of up to nine rate hikes over the next 12 months.

The strong inflation numbers coupled with a robust economic recovery and the unemployment rate falling to near a 50 year low, means the RBA cannot wait any longer to raise rates.

Many of us didn’t need to wait for the inflation figures to come out last week to let us know that our cost of living has increased. We are seeing the cost of pretty much everything increase from coffee, petrol, groceries, to clothes, electricity, child care and used cars.

Inflation is notoriously difficult to reign back in once the genie gets out of the bottle and last weeks data is a sign the inflation genie is rearing its head.

Many expect the RBA to hike the cash rate for the first time in more than a decade at its Board meeting today (3 May 2022). The first hike is likely to be a 25 basis point move, followed by a further 25 basis point hike in June.

However, there is some risk the RBA will elect to “front load” like we have seen in other jurisdictions around the world (Canada/ NZ), to get a better hold of inflation. That is being more aggressive and electing to go with an 50 basis point jump at its June meeting.

Many are expecting a further nine rate hikes, through to mid 2023. By that time, the current era of ultra cheap money will be well and truly behind us.

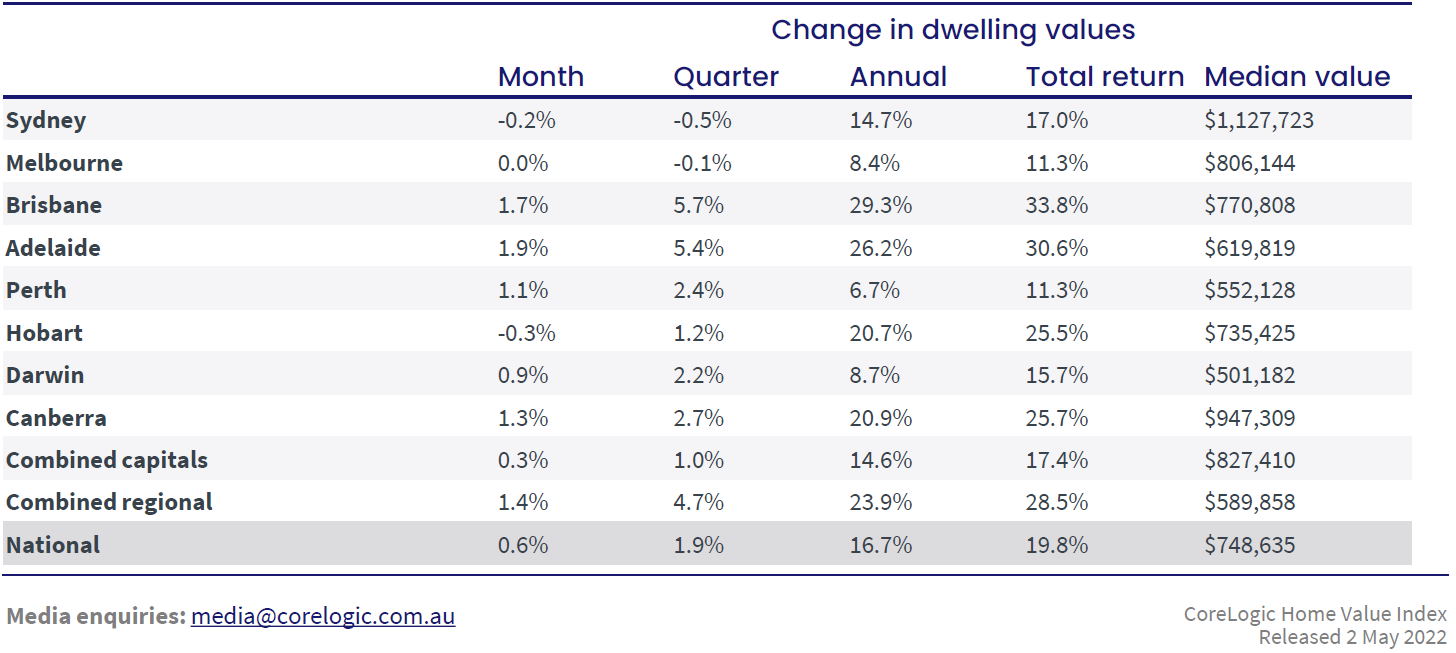

Property Prices

Canada & NZ have been leading indicators in broad terms for the Aussie property market.

Not many property spruikers will inform you of this, especially as they try to flog you their next off the plan development.

Property values do not always go up - the early evidence coming from Canada and New Zealand supports this, as some markets went from boom to significant falls in just a few months. We have seen both Canada & NZ central banks front load interest rate hikes, which has had an adverse affect on their property markets.

In Canada they have experienced a fall in property prices, with Toronto falling 9% over the past month, whereas in New Zealand, Wellington experienced a fall of 4.7% just last month alone.

These are some of the data points we have been following closely and we have been calling it out for months….that the market is changing.

We have moved from the “FOMO” buyers…

It is no longer a “runaway” property market

It is no longer a “nuts” property market

It is no longer a “normal” property market

We are in a “cooling” “slowing” “falling market”

There are pockets around Australia that will buck the trend (e.g. infill developments).

There is a lot of uncertainty around, with rising interest rates, rising cost of living, stagnant wages, and question marks over loan serviceability.

This uncertainty is reflected in the numbers, with clearance rate dipping below 60% and days on market are continuing to increase.

Now people are FOOP - the fear of over paying.

We need to be prepared.

For many it may be the first time you have needed to tighten the belt, for others your foundations are set and it is a matter of pulling the different levers in place.

However, for the past six months we have been supporting our clients with:

reviewing your mortgage

getting valuations if you are looking to invest

refinancing and considering fixing a proportion of your loan (leaving the amount you will repay over the next 2-3 years as variable)

reviewing your budget

analysing your spending and for some looking to reduce from 70-80% down to 40-50%.

establishing a buffer or emergency account

having a buffer in your offset account

reviewing your personal insurances, to ensure if you are injured, ill or pass, your family are still financially secure

In addition, the other main consideration we are currently supporting with is blocking out the white noise.

News outlets are there to sell and have a habitat of selling FEAR.

Our role is to support our clients in their financial behaviours and really take the emotion out of financial decisions.

As you don’t want to be using short term metrics to make long term decisions.

Markets

Low unemployment and rising wage inflation suggests the US economy is at a “late cycle” stage, where the risk around equities relative to defensive assets are more evenly balanced than at earlier stages of the cycle.

Due to good post-COVID growth momentum, the risk of a serious economic downturn anytime soon remains low, suggesting it’s premature to decrease exposure to growth assets.

Furthermore, the global equity outlook remains mixed, with global economic growth and corporate earnings outlook still positive, yet there is ongoing downward pressure on equity valuations due to higher bond yields reflecting the first stage of central bank tightening.

Although the US Fed Reserve is expected to lift interest rates fairly aggressively in coming months, to a degree this is already anticipated by markets.

However, as we have seen over recent weeks, volatility will remain as uncertainty continues to bubble away, as illustrated in the below “fear index” (or VIX).

Summary

In saying all this, we need to be mindful and understand:

Cost of living will continue to increase

Interest rates are expected to rise nine times over the next twelve months

Property prices will fall (there is no question if they will, it is just by how much)

Stock markets will continue to be volatile as long as there is uncertainty around

Geopolitical events can escalate and throw a spanner in the works, when everything looks and feels like it is under control.

Block out the noise.

Stick to your plan.

And remember don’t use short term metrics to make long term decisions.