Helping you navigate the uncertainty of current investment markets

Helping you navigate the uncertainty of current investment markets

How do our Lake Macquarie Financial Planning Advisers reassure worried clients when volatility returns to the markets?

Matthew McCabe, a financial planner for over 17 years, shares his experiences in supporting clients during bear markets and times of volatility.

As the recovery from the pandemic-induced recession continues, Matthew shares what he has learned from supporting clients who are feeling stressed and fearful of current market conditions.

How do you prepare your client or encourage them to have the right mindset for investing?

Being a Newcastle financial planner is not just about setting goals and hitting them. It is also about encouraging clients to have the right mindset, which is essential in their short-term or long-term prospects as investors.

A relationship built on trust is crucial, as I believe that my clients do not care how much I know until they know how much I care for them. This was something my first mentor instilled in me when I was only 18 years old.

I want to make my clients feel that I am there for them, not just for the business, but to help them long term during their life and the different stages they go through.

What’s your best financial advice to your clients during a bear market?

During this time of volatility, the best financial advice is to be calm, stay invested, be patient, and, most importantly, have a plan.

I understand this is easier said then done, however this is our role to support and educate our clients.

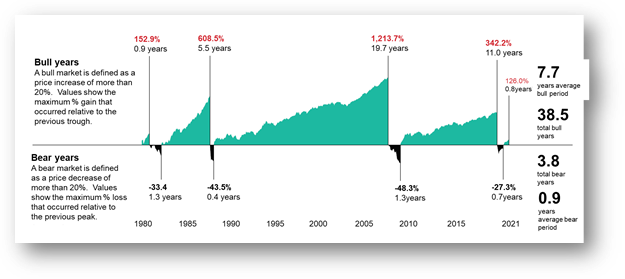

The extreme stress caused by constantly monitoring their funds isn’t worth it. I advise my clients to be patient. Experience has taught me that a bear market tends to be shorter than a bull market. Historical investment performance has a lesser impact in terms of losses than the potential gains during a bull market. Most of my clients’ investments have grown over time despite short-term volatility. Recovering from paper losses is possible once the market bounces back.

I encourage my clients to have a plan to leverage opportunities. They have to take advantage of market dips by averaging costs to add to their investments regularly (dollar cost averaging), and they could buy more units for the same amount of money when prices are down.

How do you handle it when a client’s risk appetite doesn’t match their capacity or needs?

A great financial planner has open communication, facilitating a free-flowing exchange of ideas. After reviewing sensitive private information, I would typically assess my client’s risk tolerance. Our Australian Financial Services Licence has a few questions that we ask our clients, which is meant to support us in determining where you fall on the risk spectrum. However, to be honest we generally have a really good understanding of a client’s risk tolerance from our discussions. With some of my client’s their desire to take risks is high, but their ability to handle it sometimes does not match, so I factor in personal circumstances, assets and liabilities, their money story, past experiences, past traumas, and what is required to achieve their goals.

For instance, an older client who is near retirement age doesn’t have the same degree of risk appetite as a younger person because when the investment value drops, the former does not have the luxury of time to wait for the market to bounce back, unlike the latter, who has age and time on his side to recover from losses. I guide my clients on understanding their assets and liabilities to help them determine if their status would permit them to have the kind of risk appetite they desire. Clients with high assets and low liabilities can handle risk better than those with higher liabilities as their liquidity would affect their investment decisions. Lastly, I evaluate my clients’ mental and emotional ability to handle risk. As much as we would like the performance of our clients’ investments to be beneficial to them, they should be prepared for uncertainties. If they are risk-averse, I suggest they build up their investment portfolio by positioning on the less risky investments (fixed interest) to be assured of a steady movement over time.

How does a financial advisor manage clients’ worries and expectations in an economic slowdown?

Open and constant communication with my clients is critical.

When clients’ emotions are high and influence their decision-making, I provide guidance.

The first thing that often comes to their minds is to talk to their financial advisor to confide their worries. I am there for them not only during good times but all the more during bad times.

Levelling expectations and being gently upfront from the very beginning are crucial as resolving things is a give-and-take process. Clients need to see the overall picture and understand the investment cycle process, and they need to have realistic expectations moving forward.

Generally during times of volatility we increase our market updates and client communication, to ensure the clients are informed and understand exactly what is happening in the global markets.

How do financial advisors plan for bear markets to avoid the worst impact for clients?

Bear markets are a fact of the investment cycle. Financial advisors help clients plan to avoid the worst economic impact.

As a financial planner we watch out for economic developments, such as a declining GDP, political instability, high unemployment rate, lack of investor confidence, among others.

A financial advisor should be proactive and recommend a portfolio diversification immediately to clients when a bear market is imminent to decrease exposure in volatile equities and increase holdings in bonds (unless we are in a rising interest rate environment, like we are experiencing in 2022).

Even if a bear market strikes fear among clients, there are still opportunities to take advantage of, such as dollar cost averaging. Be calm and prepare to ride the ups and downs of a bear market. For our retiree clients, we generally have 6-12 months worth of living expenses available, which ensures we are able to ride out the volatility without selling the underlying investments. If our clients still feel uncomfortable, we have an exit plan in place.

As a financial planner, we can only give advice, recommendations, and strategy advice, but the clients still have the final say as at the end of the day it is their money.