ARE YOU NAKED?

Are you naked?

Is your super fund exposed?

It is hard to hide from the news at the moment, with the constant reports of fear hitting our screens, whether that be news about Coronavirus or the massive global share market sell off.

Over the past few weeks we have seen everything from panic buying of toilet paper, the shelves being cleared at supermarkets across the country, new rules around “social distancing”, continuous rumours about nationwide lock-downs including school shutdowns, hundreds of thousands of job losses and mind-blowing amounts of government spending coupled with the lowest cash rates we have seen.

The world was not prepared for this global pandemic.

Financially this has caused chaos as people are selling assets as quickly as they can.

We have seen hundreds of thousands of people who have had their hours slashed, been “stood down” or lost their jobs over the past two weeks. Many economists are predicting this is only the start of the rise in unemployment in the country.

There were lines last week of over two hundred people at Centrelink offices around the country looking for support & handouts from the Government.

Clearly, they were not prepared. It is estimated that over 80% of Australians live pay cheque to pay cheque. This is something that will change a large proportion of the populations’ mindset post coronavirus.

No one knew this was coming.

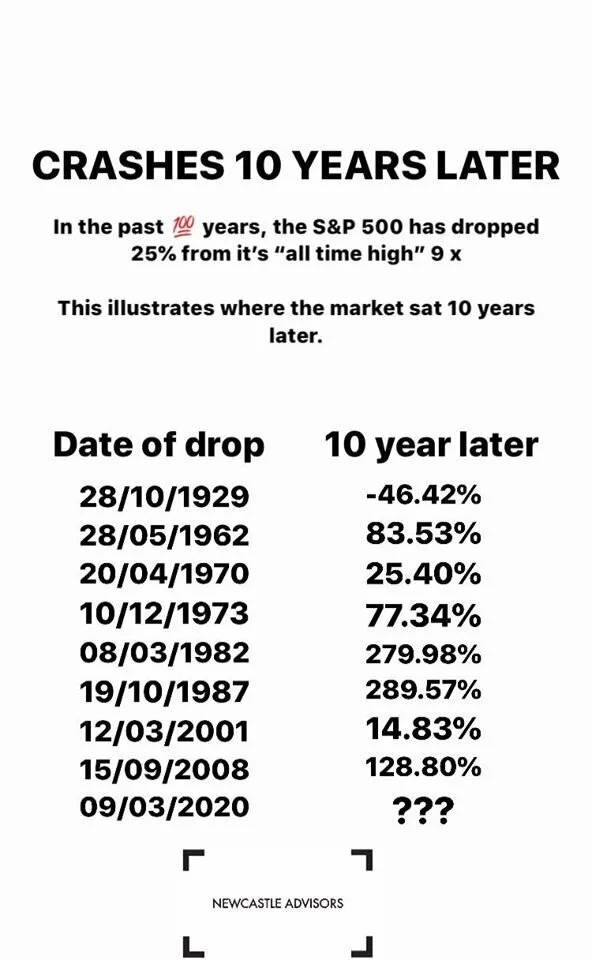

The bull market has come to an end, with growth of over 400% post GFC (on S&P 500), we have entered a bear market with the stock market sitting approximately 30% down from the highs in February.

Many portfolios – regardless of the investment mix have experienced significant falls. Over the past month, investors have experienced returns of anywhere from 0% to -49%.

The old saying goes, “don’t put all your eggs in one basket” or diversify. The concept of diversification has been around along time and still holds true today, as different assets act & perform differently to a situation.

This is why it is imperative to analyse fund managers asset allocation, as they are not all the same, as illustrated below – when comparing “Balanced” Investment Options.

Many Australians would believe a “balanced fund” would in fact be balanced. That being 50% growth orientated assets (Australian & International Shares, Property & Infrastructure) and 50% defensive assets (cash & fixed interest).

Furthermore, this is illustrated by the break up of defensive & growth orientated assets or how much you have on the table.

However, since the introduction of super ratings that have seen media outlets promote those super funds with the best performance for their “balanced” investment options, some super funds are increasing the growth allocation or risk within the investment so they can promote themselves as the best performing super fund. Furthermore, when we take a closer look, some super funds have allocated up to 93% of their allocation to growth orientated investments.

We wrote about the risk of “balanced funds” in December – stating there is no protection for Australians. However, financial planners from around the country have been jumping up and down making noise about this for the past 10-15 years.

Therefore, it is critical that you understand what you are invested in or seek advice from your Newcastle Financial Planner.

In a Australian Financial Review article on 16th December 2019 “Balanced Hostplus Fund’s risky weight weighting exposed by APRA”, Hostplus CEO David Elia said “the problem was not about classification of growth versus defensive assets, but that APRA had assumed incorrectly – that all of the funds assets were listed.”

Elia went on to say ..”previously, if a certain asset allocation had a mix of unlisted & listed assets Hostplus would report this allocation as ‘not applicable’ as they wouldn’t fall directly into a black or white classification of listed or unlisted.” He said.

“This has historically not been an issue as there was no material impact to these classifications.”

However, with the reallocation and the current economic climate many in the industry are questioning how industry super funds (with a significant proportion of their overall assets in illiquid unlisted assets like direct property, infrastructure, private equity and alternatives) will mitigate the volatility of the markets whilst meeting withdrawals.

However, in these unprecedented times many super funds have not taken into account the impact of rapid falls to the markets (Australian & international share markets, listed infrastructure index & listed property trust index all falling by over 30% in recent weeks). In addition, super funds have relied on significant inflows over many years, which have been underpinned by the compulsory Super Guarantee, with many feeling liquidity would never become an issue.

However, with many predicting unemployment to continue to rise there are a number of super funds that will find a large proportion of their members not contributing to super.

In addition, super funds did not envisage that the Government would let their members take $20,000 out of their super before retirement.

If we were to look at Hostplus for example, many of their members have been hit hardest (being hospitality, tourism, recreation and sports sectors workers), and will be looking for the Government for support via Newstart and/or a withdrawal from Super. Currently HostPlus have over 1.2m members, if there were to be 25% of their members looking to make a $20,000 withdrawal, there could be as much as $6 billion leave their super fund.

If we assume, these members are in the “balanced” investment option, Hostplus may be forced to sell down a number of their unlisted assets. However, most of these assets will include a long sales process – which may not provide the funds quick enough to meet withdrawals. Therefore, Hostplus may be forced to sell down more of their listed Australian & International shares crystallising significant losses in the meantime. Furthermore, this would completely change the risk of the portfolio, by increasing the exposure to Unlisted Property & Infrastructure and reducing the exposure to the recovery of Australian & International shares.

Remember the Industry Super Fund ad “compare the pair” well as you can see if we use what advertisements tell us we would be simply comparing the name of your investment, as the underlying asset allocation are completely different. These variations dictate the performance outcome for the specific investment.

However, as we have illustrated, it is not just the asset allocation we have to be mindful of. Over the coming weeks & months there will be a number of funds with significant unlisted investments that may significantly affect the underlying performance of your investment.

We understand lower fees are also important however the last few months have illustrated that the cheapest super fund or investment may not necessarily be the most appropriate for your specific circumstances.

On top of investment asset allocations, issues with unlisted assets & withdrawals, we have seen different investment strategies working for different clients, including a long/short investment strategy that produced a 2% positive return comparative to the benchmark falling by over 30%. However, to achieve this, the investment fee is 0.6-0.8% more expensive then benchmark or index funds.

Over the past few weeks, we have had a number of people ask us – what should we do?

The answer to this question will be different for everyone, as everyone’s situation is different, and their goals are completely different too.

However, many people that have either commented on our social media pages, or prior to social distancing had told us they had sold all their investments are sitting in cash and will invest when the market goes back up.

*30 year old who is 40 years away from retirement currently has their super invested in cash earning 0-1% per annum. In addition, we found out their mum had lost 8.5% or $16,000 in the past few weeks not 40% or $50,000 as claimed.

As the saying goes “it’s time in the market, not timing the market.”

The main reason is that nobody can time the market, if they could, they would not be working & would be enjoying themselves on their private island safely away from the Coronavirus.

Below is a snapshot that analyses the period of 1996 to 2016 for US Shares (S&P 500), which includes the Global Financial Crisis.

The graph illustrates a $10,000 investment over the period comparative to someone who misses out on a certain number of best days during the recovery.

Furthermore, this explains an investment strategy of many, sell at the bottom & buy once the market recovers.

The Australian Financial Review discussed this on 26th March 2019 in their article ‘Systemic risks are hidden in super: Murray’ where former CBA CEO, Future Fund Chairman & current AMP Chariman David Murray warned about the systemic risk of many super funds.

“My concern is, to the extent that super funds invest in unlisted, illiquid assets or that they can become forced sellers of the same asset classes of assets that banks hold for security over loan. This then sets off a spiral in the banking system,” he told The Australian Financial Review’s Banking & Wealth Summit.

“It’s also risky to assume that in a significant economic downturn that the rate of inflow will remain stable, and the right of the outflow will remain stable” he said.

This is fascinating foresight from Murray, given one year on this is exactly what we are seeing during this global pandemic. We are seeing unemployment rise & super contributions (or inflows) slow & in many cases stop.

In the article, Australian Super CEO Paul Schroder states “We’ve got some advantages in terms of the fact that people can’t draw down their money until retirement phase…”

This is no longer the case.

The Australian Government have provided Australians who have had their employment affected by the coronavirus, access up to $10,000 from their superannuation fund this financial year & $10,000 next financial year.

Mr Murray said super funds had gradually increased their allocations to unlisted investments such as infrastructure, private equity and corporate loans as they had become comfortable that continued fund inflows reduce the likelihood that they will have to dispose of illiquid assets at an inopportune time for prices below their prevailing valuation.

“So the fact that super funds have locked in the default inflows means that they feel more comfortable about taking a much longer view in their asset allocation investment strategy.”

Whatever your circumstances, ensure you understand your situation & the consequences of the actions you take.

Speak to your Newcastle Financial Planner before making any decision.

Contacting Newcastle Advisors

Cut through the noise & contact your Newcastle Financial Planner to discuss how these challenging times affect your financial plan.

If you would like further information and guidance, please contact Newcastle Advisors on 02 4963 1863 or book online.

NEWCASTLE RETIREMENT PLANNING

Supporting with all of your retirement advice across Newcastle, the Hunter, Central Coast & Sydney.

Visit our Newcastle Financial Planners at Level 1/142 Union St, The Junction NSW 2291.

Our Newcastle financial planners also have offices in Sydney and help clients across the local areas including Newcastle Retirement Planning (Merewether Retirement Planning, The Junction Retirement Planning, The Hill Retirement Planning, Bar Beach Retirement Planning, Newcastle West Retirement Planning, Hamilton Retirement Planning, Adamstown Retirement Planning, Redhead Retirement Planning, Whitebridge Retirement Planning, Kotara Retirement Planning, New Lambton Retirement Planning, Mayfield Retirement Planning), Maitland Retirement Planning (Morpeth Retirement Planning, Lorn Retirement Planning, Rutherford Retirement Planning, Aberglasslyn Retirement Planning, Metford Retirement Planning, Beresfied Retirement Planning), The bay (Medowie Retirement Planning, Fern Bay Retirement Planning, Fullerton Cove Retirement Planning, Anna Bay Retirement Planning, Nelson Bay Retirement Planning, Shoal Bay Retirement Planning, Tea Gardens Retirement Planning, Hawks Nest Retirement Planning), Lake Macquarie Retirement Planning (Cardiff Retirement Planning, Glendale Retirement Planning, Speers Point Retirement Planning, Fennell Bay Retirement Planning, Bolton Point Retirement Planning, Coal Point Retirement Planning, Toronto Retirement Planning, Valentine Retirement Planning, Belmont Retirement Planning, Eleebana Retirement Planning, Warners Bay Retirement Planning, Caves Beach Retirement Planning), Hunter Valley Retirement Planning (Muswellbrook Retirement Planning, Scone Retirement Planning, Pokolbin Retirement Planning, Cessnock Retirement Planning, Singleton Retirement Planning, Broke Retirement Planning, Rothbury Retirement Planning), Central Coast Retirement Planning (The Entrance Retirement Planning, Bateau Bay Retirement Planning, Berkeley Vale Retirement Planning, Tuggerah Retirement Planning, Wamberal Retirement Planning, Terrigal Retirement Planning, Erina Retirement Planning, Avoca Retirement Planning, Gosford Retirement Planning, Woy Woy Retirement Planning, Picketts Valley Retirement Planning) & Sydney Retirement Planning (Castle Hill Retirement Planning, Rouse Hill Retirement Planning, Dulwich Hill Retirement Planning).

Superannuation Fund, Australian Super, Aust Super, Superannuation Australia, Industry Super Fund, Retail Super Fund, Self Managed Super Funds (SMSF), Best Super Fund, top rated super funds, Retirement Advice, Host Plus, REST Super, CBUS Super, Catholic Super, QANTAS Super, BT Super, Macquarie Super, AMP Super, North Super, HESTA Super Fund, HOSTPLUS Super, MTAA Super, CARE SUPER, NGS Super, Maritime Super, TWU Super, Legal Super, Property Through Super, Superannuation Advice, Super Advice

Articles referred to;

https://www.afr.com/companies/financial-services/hostplus-has-93pc-growth-allocation-apra-20191216-p53kaw

https://www.afr.com/companies/financial-services/systemic-risks-are-hidden-in-super-murray-20190326-p517kd

https://blog.stockspot.com.au/hostplus-unlisted-assets/?fbclid=IwAR3vV_LAwWZYeNHBO_jAzwwqAjrrTABO-EQs4uZZCbVnea_l_ASoBDglFuU