RBA increased rates by 0.5% in September 2023

The Reserve Bank of Australia (RBA) have increased rates by 0.50% today (6th September 2022).

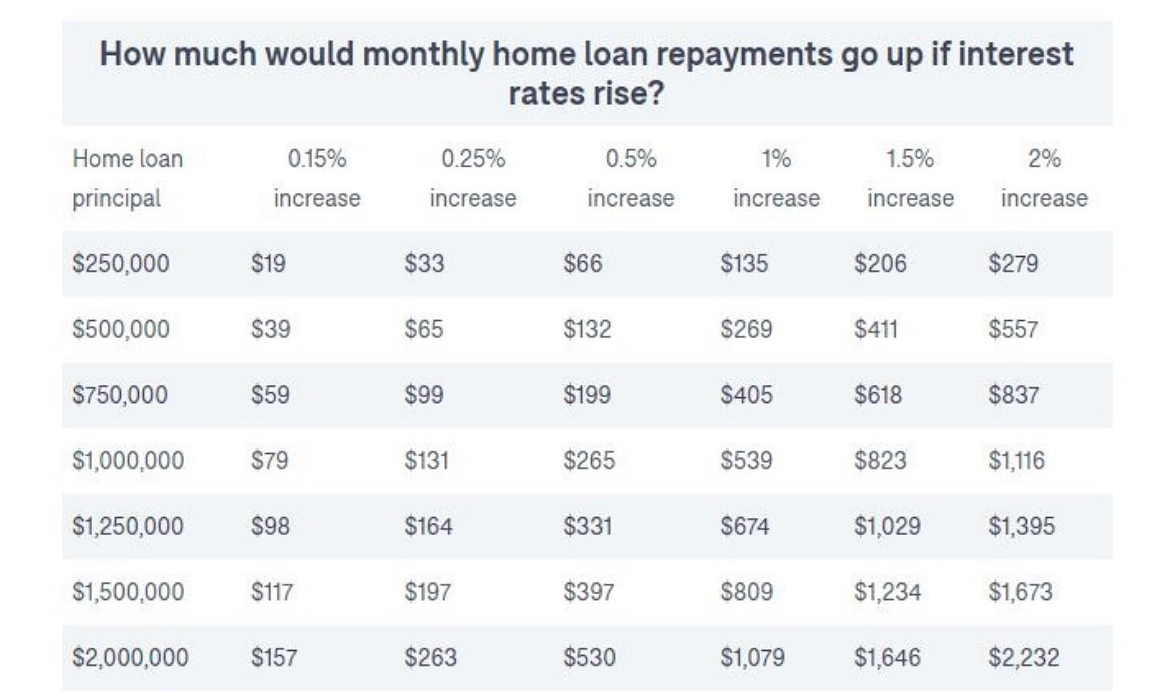

This will see an average repayment on a $800,000 mortgage rise to more than $4,300 per month, which would be an increase of $1,000 since April.

So where are interest rates going? How will this affect property prices? and are you prepared?

Where are rates going?

It has now been a week since we have had the Fed Reserve chairman Powell came out and shook the confidence out of the market, after the market was filled with optimism amid signs that inflation had peaked. Powell reiterated the Fed’s policy stance will be sufficiently restrictive to return inflation to 2%.

Federal Reserve Chairman Jerome Powell delivered a stern commitment Friday to halting inflation, warning that he expects the central bank to continue raising interest rates in a way that will cause “some pain” to the U.S. economy. Furthermore, the Fed said they would “use our tools forcefully” to attack inflation. Adding “that higher interest rates are likely to persist for some time. The historical record cautions strongly against prematurely loosening policy.”

After markets were pricing in rate cuts in 2023 after signs that inflation had peaked, Powell went on to say that the Fed will not be swayed by a month or two of data.

What are happening with Investment Markets

This has seen markets fall by 4-5% this week, as uncertainty returned to the markets and investors started to question whether we are heading for a recession.

However, one thing that is holding the markets together (at least for now) is that there is no “raw fear” of a big market collapse. As shown by the VIX (fear index or The Volatility Index) remains elevated at 25/26 - which is a number that indicates that investors should be cautious at the moment.

When the VIX jumps above 30, markets are generally in decline… and if we see the VIX venture above 40, then markets at this stage we will see some sort of total market capitulation. The last time we saw the VIX jump above 40 was back in March/April 2020 at the beginning of the global pandemic, when it peaked around 80. So for now, it is worth just keeping an eye on as an indicator.

Are we headed for a recession?

Many experts remain convinced that the Fed will have to tighten far more aggressively, which will result in a hard landing US recession in 2023.

However, when we look at the historical figures that is not always the case.

Over the past 50 years:

86% of the time after a 2-3% increase, the economy has actually grown.

17% of the time after a 3.5% + increase, the economy has grown.

So it is not a sure thing that the US economy heads into a recession. However, how far the Fed actually goes with their rate hikes will determine if they have a recession.

What rate increase can we expect?

Very interesting to see the impact that Powell’s speech had on markets over the past week.

Prior to his speech markets had priced in rate cuts of 0.75% in 2023.

After his speech, markets now have priced in only one rate cut, of 0.25% which won’t come until December 2023.

Let’s look at the numbers

2022

Rate Hikes Implemented

March 0.25% hike rate Fed Funds = 0.50%

May 0.50% hike Fed Funds = 1.00%

June 0.75% hike Fed Funds = 1.75%

July 0.75% hike Fed Funds = 2.50%

Rate Forecasts

September 0.75% hike Fed Funds = 3.25% (chances +50pt hike was 50% now 75% of a 75pt hike)

November 0.50% hike Fed Funds = 3.75%

December 0.25% hike Fed Funds = 4.00% (markets have now priced this in as the last rate hike)

2023

Feb 2023 no change Fed Funds = 4%

March 2023 no change Fed Funds = 4%

BEFORE Powell’s comments there were 3 rate CUTS in 2023 (with a -0.25% cut in May, -0.25% in July, -0.25% in Dec)

May 2023 no change Fed Funds = 4%

June 2023 no change Fed Funds = 4%

July 2023 no change Fed Funds = 4%

Sept 2023 no change Fed Funds = 4%

Nov2023 no change Fed Funds = 4%

Dec 2023 -0.25% CUT in Fed Funds = 3.75%

2024

Jan 2024 -0.25% CUT in Fed Funds = 3.50%

What does this mean for Australia?

In Australia, the RBA meet today and raised rates by 0.50%.

Experts have said that the rapid pace at which the RBA has tightened policy, overlaid with the lags between rate hikes and the cash flow impact on a home borrower, means there is a degree to which the RBA board is flying blind. It has simply been too early for the spending data to pick up the impact of the already delivered rate hikes.

There are differing views of the experts, with some saying we will need time to understand the impact of these hikes, whilst other have stated we may have seen inflation peak, however it is still not at the RBA target levels.

Therefore, some experts are predicting another 0.25% hike, whilst others have a 1.25% rise, before we may see some rate cuts towards the end of 2023 (similar to the US).

However, as we have seen over the years, often these forecasts and experts can be wrong or can change very quickly depending on what is happening around the globe. Therefore, if it looks like Australia will be heading into a recession, we may see rate cuts start to be priced in, however for now the markets have not priced in any rate cuts in Australia.

What does this mean for you?

When looking to invest, continue to dollar cost average into the market until volatility and certainty returns.

If you are looking at your home loan and freaking out at where rates are heading, the end is in sight. We need to understand that we are looking at potentially another 1.5% rate increase before rates stabilise and potentially reduce at the end of 2023/start of 2024.

Will this affect property prices?

Australians are reacting as they start to pull their belts a little tighter, this coupled with buyers continuously being re-rated is having an effect on the property markets, as many are sitting on the sidelines with the uncertainty surrounding interest rates.

We are seeing auction clearance rates falling, time on market increasing, with less qualified buyers ensuring that some vendors are taking discounts on current listed prices.

From the time the RBA slashed rates to the end of the March quarter of 2022, over 250,000 loans at a debt to income ratio of more than 6x household income were written.

So to listen to real estate agents or property spruikers regularly outline the $ value of homes that are owned outright can be misleading.

However, for generations the numbers have been pretty consistent with a 1/3 of homes owned unencumbered, 1/3 of homes owned with a mortgage and a 1/3 of Australians are renting.

These figures will obviously be skewed in the years to come, with Australia’s aging population.

However, the fact remains, that there are generation of home owners that have not experienced a rate rise, have never had to review their family budget and tighten the belt, and as illustrated above over 250,000 home owners have over extended themselves coming into a rising interest rate environment.

The housing affordability may have also contributed to Australians over extending themselves to “just” get into the property market.

Many experts are predicting further falls in the property markets.

We look to the New Zealand & Canadian property markets who have been leading indicators for us in recent months (which are down 5-6% over the past few months).

However, this backdrop will provide opportunities for many investors that are looking to invest in the property market and take advantage of some of these Australians that will find themselves in a difficult position.

Remember not to make long term financial decisions, based on short term metrics.

We need to be prepared

For many it may be the first time you have needed to tighten the belt, for others your foundations are set and it is a matter of pulling the different levers in place.

However, for the past six-eight months we have been supporting our clients with:

reviewing your mortgage

getting valuations if you are looking to invest

refinancing and considering fixing a proportion of your loan (leaving the amount you will repay over the next 2-3 years as variable)

reviewing your budget

analysing your spending and for some looking to reduce from 70-80% down to 40-50%.

establishing a buffer or emergency account

having a buffer in your offset account

reviewing your personal insurances, to ensure if you are injured, ill or pass, your family are still financially secure

In addition, the other main consideration we are currently supporting with is blocking out the white noise.

News outlets are there to sell and have a habitat of selling FEAR.

Our role is to support our clients in their financial behaviours and really take the emotion out of financial decisions.

As you don’t want to be using short term metrics to make long term decisions.