Inflation is still driving investment markets, which means a cautious approach for now.

Inflation is still driving investment markets,

which means a cautious approach for now.

The market doesn’t know if it is Arthur or Martha at the moment. It could actually be non-binary!

Towards the end of last year, the market was very bearish.

Coming in to January, hope of a soft landing returned as the Fed pivot started being priced into bonds, with equity earnings being not as bad as many experts had feared.

February brought with it the concept of no landing, as continued strength in the US labour market (employment) and inflationary pressures continued.

Then we had concerns around systemic banking issues around the globe. SVB in America and Credit Suisse. With fear, volatility and talks of a global financial crisis beginning - before central banks jumped in to stabilise and bring back confidence to the global banking system.

The next hurdle for markets will be earnings season, with equities having not priced in a recession….yet.

Volatility in the financial markets are set to continue in the immediate future, which means a continued cautious approach for now.

What’s Next?

The financial experts have considered how this plays out in 2023.

They have identified the four options available and have applied a likelihood of the scenario occurring.

A US recession is still most likely, with rising unemployment likely needed to bring down wages. Which despite the labour numbers we are seeing, we are still seeing cracks in both the Tech and Financial sectors.

US Earnings Season

As discussed above, with the chances of a US recession increasing, the focus for investors now is the impact a fall in company earnings could have on share prices.

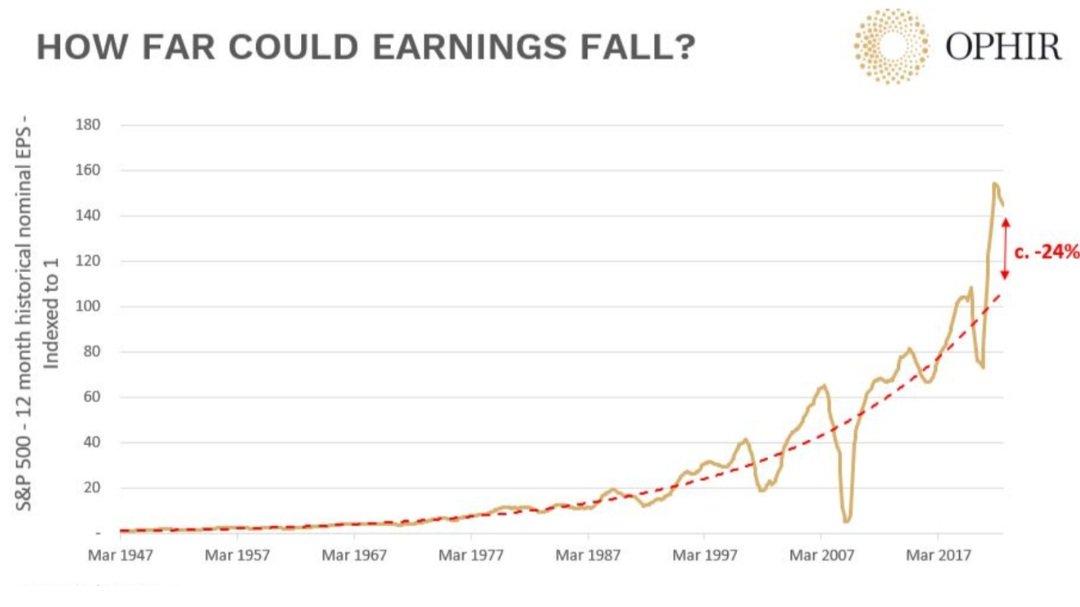

This chart illustrates that the S&P 500 company earnings are currently significantly above their long-term trend line.

Post COVID, record levels of fiscal and monetary stimulus fuelled consumer demand. Companies took full advantage by cutting costs and passing higher prices to customers helping them deliver record earnings.

We have been saying this since October 2022…

However, how far could company earnings fall?

If you follow market forecasters, they are predicting on average that S & P 500 earnings will fall during 2023 by only -1%.

This seems very optimistic when you consider the average S & P 500 earnings fall during a US recession is -13%.

The market is certainly taking a glass half full view at the moment, with equities having not priced in a recession (yet).

The next big test is when the US reporting season kicks off in April.

Australian Inflation

We saw CPI inflation fall for the second consecutive month.

A sharper than expected fall in annualised inflation has supported mounting expectations of a pause to the Reserve Bank’s monetary policy tightening cycle.

According to the Australian Bureau of Statistics’ (ABS) latest monthly consumer price index (CPI), annualised inflation fell for the second consecutive month to 6.8% in February - below market expectations.

This represented a 0.6% decline from the previous month, in which annualised inflation was reported at 7.4%

Interest Rates & Property Prices in Australia

Financial experts are split on whether or not we will see a 0.25% interest rate rise in April (next week).

Inflation is still significantly high, however we are starting to see the data and feel the effects through the economy. The question is, is this happening fast enough for the RBA?

Our view is that rates will be placed on hold, as we continue to see more and more data, and the affects we are seeing through the economy.

However, this could change quickly with Government policy and intervention, through determining award wages, power and gas policy, carbon reduction pathway, and potential new regulations for the big banks, which can significantly affect the direction of inflation.

Property prices continue to see downward pressure.

We have seen lower than average flow of fresh stock (houses for sale) added to the market, which has been the key factor supporting housing values.

Over the past month, the CoreLogic Daily Home Value Index has shown in some cities a lack of new stock, which has stemmed the decline in values.

Sydney housing values in particular are up 0.9% over the past 28 days just as the volume of new listings falls almost 40% year-on-year.

Watching the ebb and flow of new listings will be a key factor in the performance of this year’s housing market.

Arguably there has been an accrual of pent up supply since September 2022 as prospective vendors delay their selling decisions, possibly frustrating buyers with a shortage of options.

However, any sign of rebound in new stock on the market could trigger renewed downwards pressure on housing values, unless the increase was absorbed by a commensurate uplift in buying activity (which could be unlikely, given where interest rates are at).

Australian Economy - Snapshot

While inflation looks to have peaked, it could become sticky in some economies.

Doubts remain as to whether central banks can engineer a controlled reduction of inflation pressures or whether their actions overshoot and create demand destruction and a deep recession.

We are starting to see that rate hikes are starting to bite. We have seen this on the streets for a number of months, with the data lagging what affects are happening.

Aside from inflation, the other growing concern for investors is government policy intervention in business.

As investors shift their focus on to the practical reality of the market environment we are operating in, we are seeing one key shift that several companies are referencing the growing influence of government policy on their outlook.

Investors should be aware of government influence over the companies in their portfolios from four perspectives:

determining award wages

industrial policy, including regulating the big banks

power and gas policy

the carbon reduction pathway

Ensure you understand your investment strategy and portfolio.

Understand how the volatility will affect your portfolio.

There will be further opportunities in the coming months.

Within the equities market, we will see further earnings pressure as companies start to price in a recession.

Within the property market, we will see further pain with the higher interest rates (and mortgage cliff) starting to have full affect.

Ensure your financial plan is up to date and ready to take advantage when opportunities arise.

For those long-term investors, come back to your long term goals.

It will not feel like it at the time, however this uncertainty will pass, interest rates will stabilise (and potential fall towards end of 2023/ start of 2024) and so will property prices.

Over the pass 30 years, the median value of Australian dwellings have grown 6.80% p.a.

Over the pass 20 years, the value of a diversified balance portfolio has returned 6.60% p.a.